There are so many opinions on whether or not you should pay off your mortgage early. Some say that paying off your mortgage is a bad idea because you could make a lot more money in the stock market. With the incredible stock market returns over the past decade, there’s a lot of truth to that. And others appreciate the peace that comes with not owing anything to the bank each month. The benefits of a paid off house are hard to deny as well.

So, what’s the right answer?

I’m not sure there is one. I think only YOU can decide what’s best for YOU.

In 2013, my wife and I decided to pay off our $200,000 mortgage in less than 5 years. It was an aggressive decision and one that required a lot of partnership and dedication. But we did it … together. And we’re so glad we did.

That was a personal choice and it was best for our family.

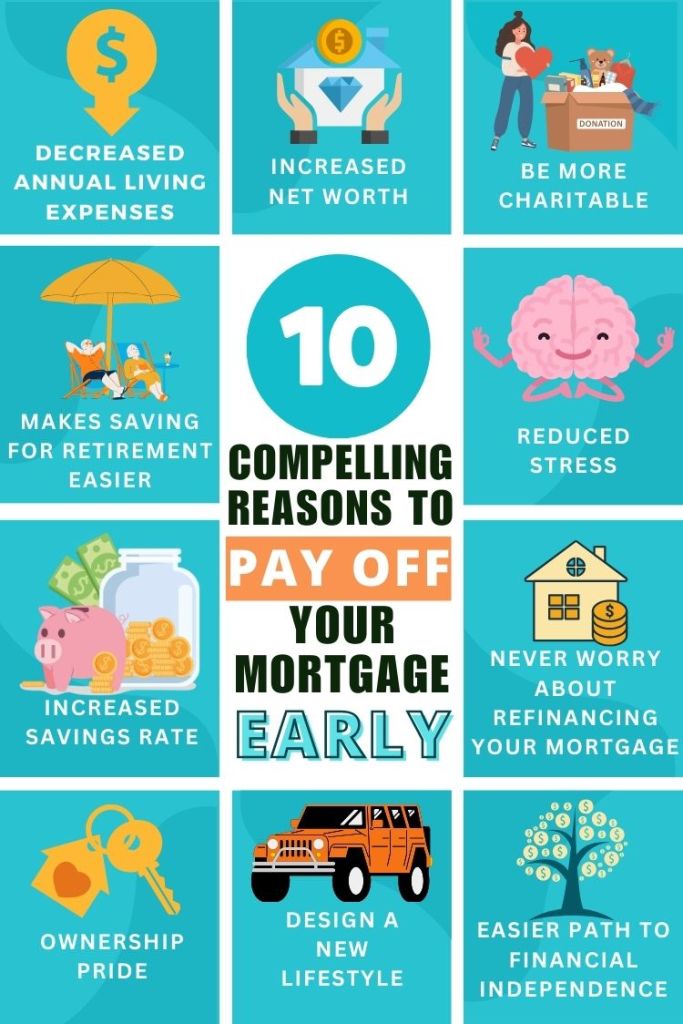

Top 15 Benefits of a Paid-Off House

If paying off your mortgage sounds interesting to you, here are 15 compelling benefits of a paid-off house.

1. Decreased Annual Living Expenses

According to the US Department of Labor, the largest expense in the typical American family’s household budget is their mortgage or rent. Imagine that being completely wiped from your annual expenses. What a weight off your shoulders!

That would leave you more money for fun, vacations, investing for the future, contributing to your kid’s college funds and so much more.

Since our mortgage and extra principal payments were around 35% of our living expenses, we are breathing MUCH easier with our mortgage gone.

2. Makes Saving for Retirement Easier

Before paying off our mortgage our annual expenses were around $75,000 per year. With that type of lifestyle, we would need to save around $1,875,000 to retire comfortably using the 4 percent rule.

By removing our mortgage from the equation, our annual expenses got to around $60,000 per year. In theory, this means we would only need to save up to $1,500,000 for retirement to live a comfortable lifestyle.

Now there are a lot of factors that can throw that convenient math problem off (inflation, lifestyle change, etc), but when all is said and done, it’s going to be easier for us to retire. $375,000 easier!

3. Increased Savings Rate

With no house payment, we were able to save around 50% of our income. That was huge for us.

At the beginning of our marriage, we were living for today, spending what we wanted and we were happy … until we realized we had a negative net worth. Yikes!

Having a large cushion of cash, built-up retirement accounts that have allowed us to achieve Coast FIRE and the ability to funnel more of our money toward income-producing assets also makes us feel happy … just in a different way.

4. Increased Net Worth

When you don’t have debt, you avoid the negative drain on your net worth. And without a mortgage, this is doubly true!

When we started our journey of financial betterment in 2010, we had a -$50,000 net worth. (Yes, that’s a negative symbol).

We owed A LOT more than we owned. I owed more on my home than it was worth, had $30,000 of student debt and I was spending more than I was earning. I even bought my wife’s engagement ring with my student loans!

10 years later, our net worth grew to over $1,000,000 through simple investing strategies, increasing our income, and focused debt destruction. Without a mortgage, our net worth continued to soar.

(I track our net worth with a simple spreadsheet, but an awesome tool to automate the process is a free service called Empower.)

5. Have More Fun

My wife loves to do design projects in our home. I love vacations. With more available cash flow, we’ve been able to enjoy life and reward ourselves more lately.

Nicole has been able to update our laundry room, update our kitchen, buy new furniture guilt-free and we even got the big screen TV we always wanted. This home now feels like a palace and it’s ours!

We’ve traveled a lot more as well. Disney World, Cabo San Lucas, Los Angeles, Ft. Lauderdale, Cancun and many trips to Northern Michigan have been some of our favorite destinations since paying off our mortgage.

Having the extra cash available has helped us travel without restriction. Getting out of town during our Michigan winters is now a must for this family.

6. Reduced Stress

I don’t know about you, but I got really stressed out about the size of my mortgage. Having such a large payment each month made me feel worried.

- “What if I lose my job and we’re not able to make the payments?!

- “Or what if I get a new boss and he’s a complete jerk, but I can’t leave because of the mortgage?!”

- “What if a recession rolls in and severely impacts our income?”

These were real reoccurring thoughts I had. And I couldn’t just tell myself to calm down or not think about it. (Believe me, I tried. The Calm meditation app has become a good friend of mine lately!)

When our $1,300 (w/o taxes and insurance) payment was gone, my stress level decreased dramatically.

Sure … There are still other bills we have to pay for the rest of our lives, but none will ever be as large as our mortgage.

7. Never Worry About Refinancing Your Mortgage

You know when the interest rates drop and all you hear is chatter about refinancing your mortgage? Well, when you don’t have a mortgage, you don’t even have to wrestle with the decision of whether you should refinance your mortgage or not.

That is one less decision you have to make FOR THE REST OF YOUR LIFE!

There are major benefits to reducing the number of decisions you need to make in your day. You’ll be more productive, your mind will feel clearer and life will feel easier.

8. Ownership Pride

The fact that Nicole and I own our home outright fills me with so much pride. The peace of mind that comes with true homeownership is incredible.

I’ve even found myself standing on my front lawn staring at my house and saying, “That’s our house. We own all of it. My kids will always have a place to call home.”

Those statements are REALLY fun to say.

9. Design a New Lifestyle

I’ve had the chance to interview dozens of families on my podcast who have paid off their mortgages. One of the most impressive things I’ve learned about how mortgage freedom has changed things for them is their overall lifestyle design.

Many have gone from working full-time jobs to just part-time jobs. Now that they don’t need as much money to live, they don’t want to work as much. How cool is that!?!

Others completely changed career paths altogether. It’s as if they now had the confidence and financial cushion to make bolder lifestyle decisions. That’s what mortgage freedom did for them.

Like these folks, I made the choice recently leave my corporate career and work part-time as a family finance coach and a full-time Dad. It's been a wild ride so far, but I'm loving it.

As for my wife, she recently left her 9-to-5 lifestyle to go back to school and become an esthetician. She's now working part-time too!

Not having a mortgage definitely gave us the confidence to take those major lifestyle leaps. This is MY FAVORITE benefit of all 15 benefits of a paid-off house.

10. Easier Path to Financial Independence

With a paid-off mortgage, you don’t have to save as much money to reach financial independence. Your expenses are now significantly lower.

For example, if your family spends $84,000 to live each year and then pays off your mortgage with a $1,000 payment per month (principal and interest only), your new annual living expenses are only $72,000.

That means, you now only need to create $6,000 in monthly income to become financially independent.

How can you get there? Here are 5 of my favorite income-producing routes:

- Buy-and-hold rental real estate

- Investing in a taxable brokerage account

- Affiliate or advertising income through a blog or YouTube channel

- Two spouses working part-time at home

- Starting your own work-from-home business

I’m not insinuating that people shouldn’t focus on these income routes before they’re mortgage-free. In fact, I’d highly recommend it!

If you want to get into rental real estate, more power to you.

Have a small business idea that allows you to follow your passion and provide for your family? Go for it!

Nicole and I have had a lot of trial and error to get where we are today. The knowledge we’ve gained from that trial and error has been priceless.

Of course, you don't want to just take our word for it. Over the years, I've heard dozens of stories of mortgage payoff journeys. So I thought I'd share five of my favorites and what they consider to be benefits of a paid-off house.

11. Be More Charitable

Keith Robinson and his family are also mortgage-free. Living in California, they know a thing or two about the high costs of living. That's why Keith reframed his attitude. By “saying yes when others say no”, he was able to supercharge his income as a jail deputy.

He and his wife worked out a schedule that allowed him to accept as much overtime as possible. By clocking hundreds of hours of overtime and working hard, he snagged some promotions and doubled his income. All of this allowed the Robinson family to pay off their mortgage early.

One of the biggest benefits of a paid-off house from their perspective is that it allowed them to be more charitable. They made giving a priority even when they were in debt. However, being mortgage-free means that they have even more money to support causes they care about.

To hear more about the Robinson's mortgage freedom journey, take a listen here.

12. Inspire Generational Wealth

Marriage Kids and Money is all about strengthening family trees. Did you know that paying off your mortgage does exactly that? Take the McCoy family for example.

To fast-track their debt-freedom journey, the McCoys started flipping houses. It became a family affair. In fact, one of their kids even tried to use their after-school visits to the home improvement stores as an excuse to dodge a homework assignment!

By involving the kids in the flipping process and also having them help color in mortgage payoff tracker boxes, the whole McCoy family really invested in the process. They started having conversations with their kids about what money means and the different trade-offs they could make.

Choosing to be debt-free sends a powerful message to kids. And as parents know, they're always watching and learning from us. Involving them in a financial milestone like a paid-off house can set the tone for how they view money later in life.

The McCoy's whole mortgage freedom story–including all their trips to Lowe's–is available here.

13. Dream Bigger

A friend and fellow blogger Jessi Fearon is also mortgage-free. She and her husband decided to completely pay off their home…and they did it on an income of less than $50,000 a year!

One mistake people make is thinking that if they don't have a big income, they can't tackle big debt. That's not the case! Of course, earning more money can make paying down debt easier. But if you're committed like the Fearon family was, it is possible to pay off your mortgage early.

This huge undertaking taught the Fearon family a lot of things. Learning to dream bigger is definitely one of the benefits of a paid-off house. The Fearon family knows that being mortgage-free will allow them to be more flexible with their spending. That means taking family trips now and tackling her husband's big dream of building a home from the ground up in the future.

Find out more about how the Fearon family paid off their mortgage early on an average income here.

14. Show Others a New Path

If you listen to Americans talk about money, the mention of a mortgage isn't far behind. For better or for worse, debt is part of our cultural narrative. The McNeely family takes issue with that.

The founders of His and Her Money set out to prove that an average couple could live a life without debt. That's exactly what motivated them to slash their mortgage as a single-income household. Once they developed this vision of debt-free living, they became laser-focused on the task. Tai would rearrange their budget or sell something, immediately sending that money to the mortgage. Even $20 here and $50 there helped chip away at the interest calculations. The amortization changes motivated them to push through any burnout they were feeling.

They are motivated to show not only their kids, friends, and family how life looks when you take a different path. They are also motivated to help as many people as possible imagine a different trajectory for themselves. Being mortgage-free allows them to live that example. It also allows them to work for themselves, growing their business to inspire others.

To check out the full scoop on how the McNeely family paid off a $330,000 mortgage in five years, click here.

15. Grow Rental Income Opportunities

Christina Marriott knows a thing or two about the benefits of a paid-off house. How come? She and her husband are working on paying off their third and fourth mortgages!

In addition to a primary residence, the Marriotts also have three rental properties. These rental properties are the key to their long-term plan. The rentals are a form of passive income for the Marriotts. They only invest in properties that net at least $1,000 a month. Currently, all of the cash flow is redirected into paying off the rental properties, which is how they've expanded the number of doors they own.

Of course, Christina also points out that as exciting as it is to own a rental property free and clear, there's nothing quite like paying off your primary residence. She says that feeling was actually the best.

When they are entirely mortgage debt-free, they will reconfigure the cash flow from their rentals. This cash flow will allow them to take one to two years to make some lifestyle upgrades. Christina has her eye on a new kitchen and knows that they both need to trade in their cars soon too. After that, they will use the cash flow to allow her husband to move to part-time work.

Find out more about Christina's journey to be mortgage-free on an almost half-a-million-dollar home in her 40s here.

Final Thoughts on the Benefits of a Paid-Off House

In the end, the plan to pay off our mortgage has worked out very well for our young family. Being mortgage-free at 35 was a family tree-changing moment for us.

Not everyone thinks these 15 benefits of a paid-off house are worth it. And that's okay! For some people, it makes more sense to prioritize other money goals. The important thing is that you find a path that works well for your family.

If you're inspired after reading through these benefits of a paid off house, check out our mortgage payoff calculator to see how extra payments can accelerate your journey to complete debt freedom.

Carpe Diem Quote

“The goal isn’t more money. The goal is living life on your terms.”

Chris Brogan

What do you think of these benefits of a paid-off house? What would you add to the list?

Do you think paying off your mortgage early is not a good idea?

Please let us know in the comments below.

45 Comments

Hello! Great article!

I live in what I consider a ‘starter home”..

Not my dream house, but certainly a great place to live. My husband and I have been saving to purchase a new home, somewhere with more land where we can build a homestead. We have been searching for 2+ years, but with the crazy housing prices and rising interest rates, I’m debating whether to stay where we are as we have saved enough to pay off our mortgage.

Any advice? Debt free in our non-dream house our dream house with hundreds of thousands in debt? Thanks!

Just ask Dave Ramsey what he thinks about “dream homes.” He says they’re an excuse people make to overspend on a house. Pay off your house, enjoy living without a mortgage, and save as much as you can to quickly move into a new property.

Thanks for the great points and insights!!

Thank you!

PAID MY MORTGAGE OFF IN 2018. I AM 35 NOW. I AM JUST RACKING UP ALL MY PAYCHECK. I HAVE BEEN INVESTING ALOT NOW. AND SAVING AS WELL. IT FEELS AMAZING. I BOUGHT A BRAND NEW ELECTRIC CAR FOR CASH. IT’S A GREAT WORRY FREE LIFE.

For me, the biggest benefit of paying off early is the liberty of not needing such a high cash flow in the years that follow…knowing that if I want to switch careers, take some significant time off in my 40s — my overhead is sufficiently low that I can weather most choices. For me, it’s always been part of my risk tolerance. I value the future enough to max out ROTH/IRA options…but value the present and short term liberty enough to make paying off the mortgage a goal even at the expense of taxable investments. I don’t do bonds in my investment accounts but am grateful for the buoying effect home equity has during market downturns. Knowing that my near term cash flow requirements will be halved makes any mental anguish over not growing a sizeable taxable brokerage tolerable. I feel like I’m paying for my future freedom…my future options in lifestyle. Investments do that but timing/matching an investment’s payout/drawdown w/ your life stages/goals makes this make too much sense for me. I’ve chosen not to pay down so quickly that I jeopardize my emergency funds and cash reserves — present ability to weather whatever life throws at me. I expect to make my last payment next month. I don’t expect life to change immediately but I do hope and expect there to be more courage for choosing the life and lifestyle I value and have been positioning for over the past two decades.

Hi, Andy! I love this article and your accompanying video. My husband and I got a later start to paying off the mortgage, but I am laser focused and plan to have it paid off by next year for my 50th birthday.

One thing that never seems to be mentioned in paying off the mortgage and FIRE community are blue collar workers! My husband is a truck driver, and I am well paid with an Associate’s Degree in an industry that may soon be deemed redundant. If that happens, I have no training or education for anything else, and we’re both going to be in our 50s with young kids. My husband is looking at a knee replacement. Not a big deal, per se, for anyone else, but he’s carrying our insurance, and what happens if surgery doesn’t go well and he can’t climb 3′ for getting into his truck to drive 6-8x a day and then get back up to offload his freight?

My uncle is a plumber with a blown back and knee, working very part-time in his late 50s and into his 60s.

My aunts were nurses making bank — until they blew out their backs with patients falling with dead weight on them.

Sooo many FIRE folks espousing investing like crazy versus paying off the mortgage work white collar jobs with fat salaries.

This is just our family’s scenario, but coming from blue collar/skilled trades, I want the house paid off and we will go crazy saving for retirement next. Everything is rosy when you’re 25-35 in peak fitness and energy. I will sleep much better when our expenses are way lower.

Also, take the vacations while you’re young and fit enough to enjoy making those memories. You won’t regret it.

Such a great point! Having your home paid off is a beautiful thing. It can help you rest easier.

Starting early with investing can help you get the most bang for your buck because compound interest works best when it has time on its side.

If you’re able to invest some while paying off your mortgage, that is the best of both worlds in my opinion. That way you have some income to use in retirement.

What do you think about not having mortgage interest deduction on tax return?

Hi Diana! Thanks for asking!

I answered your question here: https://marriagekidsandmoney.com/podcast/keep-mortgage-for-mortgage-interest-tax-deduction/

Thanks again!

We’re on our way to be mortgage free in 6 years. I’m 55 and my wife, of course, will always be 29. But we are looking forward to it!

#2,3,4 and 10 can be disproved with simple math. Paying off a mortgage that has an interest rate of 4% vs investing your money into an index fund that will, on avg., get 7% after inflation is never a better investment, mathematically speaking. 7% is also a very conservative ROI expectation that should serve as every persons discount rate. By paying off your mortgage you are buying a 4% ROI for your money, which by any investment standard is quite poor. Now, the psychological benefits espoused in your article of being debt-free are spot on,no disagreement there.

Glad we could agree on one part of the article!

Actually with the math, It makes sense to pay the mortgage off first then invest. He did it the right way. Now he doesn’t need to worry about job loss or have stress. Now he can use his paychecks or whatever income to build wealth. Don’t be jealous because he did it and you haven’t .

Hi Dale,

1) You’re assuming we don’t end up in a recession long-term.

2) You’re assuming we don’t have years upon years of inflation.

3) Interest on a mortgage makes ZERO return. You’d literally have a better probability of making a profit by taking that money and buying lottery tickets with it.

4) Capital gains on mutual fund sales are taxable.

5) You’re assuming that people with a mortgage will be able (and willing) to keep working, won’t have huge unexpected expenses, and will be able to actually make their mortgage payments in what is commonly their old age as they slave away on their 30-year bloated mortgages as they struggle on a fixed income.

Hi Andy,

I’m a real estate Broker in California. My experience with buyers (having helped hundreds purchase a house) is they routinely borrow as much as the bank says they can ‘afford’. Banks don’t know what you can afford, only how much they can lend you. It doesn’t mean you are going to like living with that mortgage payment. A buyers happiness is not a factor in their equations. What you can afford on a house has more to do with the kind of life you want to live and what you value most. I appreciate your sentimentality surrounding home ownership as I once felt that way. I have seen (and made) poor choices surrounding house purchase decisions that are fueled by these sentiments. The statistics are that 78% of working Americans live paycheck to paycheck and half of all marriages end in divorce. I’m convinced there is a connection.

When house shoppers are in house hunting mode, they somehow feel they are buying the life they dream of and the time, money and energy to live it. In fact, I have found that by over committing resources to a house they are, in fact, undermining what they want most. A happy home.

The best shot for paying down that mortgage early, is don’t get into too much mortgage in the beginning.

I enjoy your posts. I think you are giving good advice at an important time as young families invent themselves.

Bill

Thank you for that feedback Bill! Being a real estate agent, I’m sure you’ve seen a lot of home purchases and a lot of mistakes as well.

My first home mortgage took up around 70% of my income each month … I hated living like that and vowed to never do it again.

I believe paying your mortgage is absolutely the right way to go Andy. I have several years ahead of me but last year I paid a big lump sum to reduce my balance. I don’t regret it a bit and look forward to the next lump sum payment that will take me closer to freeing myself from that debt. The sooner your mortgage is paid, the sooner you have an asset and not a liability!

I love it! I’m glad you have clarity around your goals. Contact me when it’s paid off because I love sharing stories like yours on my podcast.

Agree with Lance that its a very personal choice. Being debt free at the cost of forgoing a couple of percent extra return you could have had if you chose to keep your mortgage always works for me. It also reflects the mindset of financially independent people who want to live within their means and not spend more than they can reasonably afford.

We definitely took the emotional choice over the mathematical choice, but we’re happy with our decision. Less stress wins for me every day.

Andy, this is my current goal in my experiment. We (my wife and I) decided this year to focus on paying off my mortgage for many of the reasons you mention. It’s great to see others have the same doubts (e.g. should I be investing more instead) I’ve been experiencing but ultimately I think it’s the right decision. My current goal is to be completed in 6 years, but I think I can do it significantly faster. #7 is probably the main driver for me and the wife with #2 being a close second. Once paid off, we own our home outright with no debt. Looking forward to your celebratory post!

This is awesome Gabe! You’ll be surprised at how fast it flies by when you have intentionality and automation backing you up. I predict you’ll be done in 5!

I think debt payoff is a extremely personal choice. Sure, the numbers almost always work out better in the long run if you invest instead of pay down debt, but it’s the mindset of being debt free and not being shackled. Excellent work!

Thanks Lance! Nearly there. You are absolutely right. It is all a personal decision. We should all do what’s best for our individual situations.

We are paying off our 30 year early, on track for approximately 17 years total. For us, we want to still focus on investing right now, but paying off early will allow us to be mortgage free before our son is in college. Here’s to sticking to the plan!

Completely agree with that sentiment! Do what is best for your family and you can’t go wrong.

Congrats on being so close to being done! I think you’ve got all the right reasons listed here. We were aggressively paying down our mortgage before we decided to downsize.

We recently bought land with cash and plan to build small (1000 sq ft for a family of five). Our hope is to build with a small mortgage and pay it off within a couple years. We’re technically debt-free right now but paying rent. Can’t wait to get to the point where our only housing costs are property taxes and maintenance!

Your plan sounds awesome! The 5 of you are going to make some incredible memories at that house. Best of luck with the build!

When your kids go to college, the FAFSA will create an EFC which is an estimate of the amount of money your family can pay for college. Home equity does not increase your EFC. Money in stocks or rental properties does. If your income is high, it won’t matter much, but it might have helped me out to own my house free and clear instead of having money in mutual funds.

Wow! I never thought of it from that perspective. College costs are going to be massive when our 3 and 5 year old grow up. Building up the 529 as we speak!

The 529 will count against you on the FAFSA. It is counted as a parent asset and 5.6% of its value is added to your expected family contribution. If you are not already maxing out a Roth-IRAs, they might make more sense than the 529.

We’re maxing them. Is your thought to only use the Roth IRA contributions to pay for college as opposed to 529 savings? Interesting!

The Roth does not count on the FAFSA because it is a retirement account. If someone is not taking advantage of a Roth IRA, it might make more sense than the 529. The contributions (but not the gains) to a Roth IRA can be withdrawn without a penalty.

Thanks for the clarification!

I’ll admit that I wasn’t so sure about this post when I read the title, but I like your reasons. You are approaching it from the right mindset, and that’s all that matters. And great job paying it off so quickly! Just that alone is something to be really proud of.

Thanks Dylan! There are tons of ways to allocate your money, right? If we educate ourselves properly, we can make the best decision possible that fits our specific situation. I hope your Trail to FI is going well!

Wow congrats on knocking off soooooo much of that mortgage! My wife and I are tackling our student loan debt and we hope to have that paid off within the next year or so.

It’s like a domino effect Eric. Once you knock down one debt, the debts that follow are that much easier because of the momentum you’ve built up. I really appreciate the kind words and encouragement. Good luck crushing those student loans!

Great list, Andy! Yes, stick to your guns and you’ll be celebrating soon. I’m working on mine too.

Thank you for the encouragement Amy! I always knew you weren’t a suspicious bot ;)

See you in Dallas soon!

We paid off our mortgage three years ago and haven’t had a single regret about it! We’re so happy we took that step – even though we had a low (~3%) rate.

So glad to hear you say that! Thank you for the encouragement Brad!

It might have been a low interest rate, but you are guaranteed that you’ll never have to pay it again.

That is awesome! Only 20k to go! That will be such a huge accomplishment. I love it when you said no one can take your house from you – ever. That’s amazing!

Thanks so much Cat! It’s been a long road, but we’re nearly there. Then onto the next steps!!