Some folks are feeling uneasy about investing. Uncertain times can create nervous investors.

Colin is one of those folks. He asked this question about investing in a Roth IRA:

“Before the war, I was planning on setting up a Roth IRA for my wife. But now with the economy on a downward slope, I was wondering if I should wait a little bit or get in now. What you do think?

Colin, thank you for reaching out about investing during uncertain times like this.

This Russian invasion is horrible and I’m hopeful the world will continue to support Ukraine as it has been over the past month.

Let’s discuss your question … Is now a good time to invest?

Well, let’s assume you and your spouse are in your 30’s (based on your Twitter profile, that appears to be the case).

I’m going to share 5 reasons why NOW is a good time to invest. And even if someone’s listening to this after the war is over … it’s still a good time to invest.

Why NOW is a Good Time to Invest

1. If You Wait For Things to Get Better, You’re Buying Your Shares at a Higher Price

Uncertain times can be difficult for investors. This is your hard-earned money after all.

Realize though that if you decide to wait until things get better in the stock market, then you’ll be buying your shares at a higher price. When you do that, you’ll be getting fewer shares and in the long run, building less wealth.

Let me give you an example:

VTI (which is Vanguard’s ETF that covers the Total Stock Market) is currently valued at $227 per share (prices fluctuate so be sure to check before investing).

The last time it was valued this low was in last summer. So if you buy at today’s prices, you’re essentially getting it at a discount.

Shockingly, that low price of $227 was an all-time high for this fund! So, I don’t doubt that we’ll be hitting another all-time high again really soon.

Will it be this year or next year? Well, let’s discuss that in our next point.

2. No One Knows What the Stock Market Will Do This Year

Ignore all of the financial news experts that tell you what is going to happen with the stock market this year. Do you know why?

Because they are guessing. They have no idea what the stock market will do this year. Their living is made from making guesses all day long. They may be educated guesses, but they are guesses nonetheless.

Since they don’t know, you don’t know and I don’t know … we just need to start as soon as possible.

And we need to realize that the stock market will go up and down like a roller coaster for the next few decades until you reach retirement. BUT over that timeframe, historically, it’ll more than likely go up.

3. The Stock Market (Historically) Goes Up in the Long Run

Does it return that every year? No, but on average, over the decades, your ability to stay in the market in good times and bad can yield a 10% return.

So even if times are uncertain today, investing today, instead of tomorrow or 1 year from now, will get you in the investing habit and take advantage of time.

This may be one of those moments where the stock market is down. That’s good news for new investors because you’re buying your shares at a slightly lower price.

4. Investing Favors Those Who Start Early

The earlier you can invest, the more wealth you can build. Let’s do an example that demonstrates “waiting to invest” for the right time.

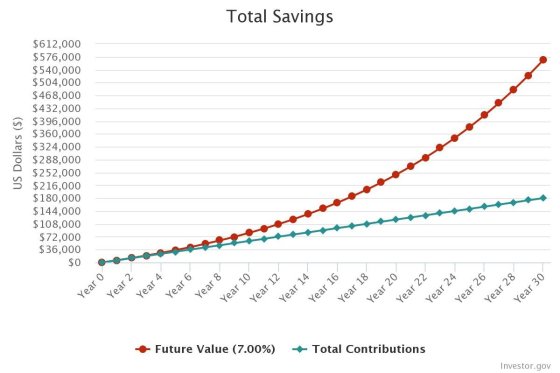

$500 Invested in Total Stock Market for 30 Years

In this hypothetical example, your wife is 35 years old. She starts investing in a Roth IRA today with $500 per month in a total stock market fund like VTI. 30 years later, she could potentially have $566,000 factoring in inflation.

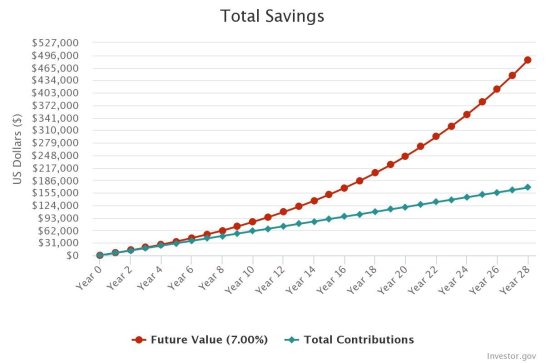

$500 Invested in Total Stock Market for 29 Years

Let’s say she waits just one year to start investing in her ROTH IRA. Her total drops to $524,000. That delay costs her $42,000!

That gap grows even larger, the longer you wait.

$500 Invested in Total Stock Market for 28 Years

Let’s say she waits two years to start investing in her Roth IRA instead of starting now. That new total drops to $484,000. A delay cost of $82,000!

My point is … start investing early and don’t delay.

5. Dollar-Cost Averaging Makes it Easy

Deciding when to get into the stock market can be really stressful. That’s why concepts like dollar-cost averaging allow you to relax and let the market do its work.

Dollar-Cost Averaging is an investing strategy that allows investors to invest equal amounts periodically no matter what is going on in the stock market.

For example, your wife investing $500 per month for the next 30 years, no matter what, is Dollar Cost Averaging.

Over time, this has been proven as a solid and effective strategy for long-term investing success. If you allow automation to take care of the process for you, then you’re not tempted to stop your dollar-cost averaging plan.

This way you’re buying consistently over time. You’re buying in good times and in bad times. And you’re allowing yourself to ignore crazy market cycles and difficult global news.

By ignoring that news, you can focus on what matters most … your family and personal life goals.

Reasons You Shouldn’t Invest Now

I’m a big proponent of investing, but there are times when you should consider holding off on investing. Here are a couple of reasons:

No Emergency Fund

If you have no cash saved up for emergencies, you are setting yourself up to go into credit card debt if any emergency arises.

I’d suggest holding off on investing until you have at least $2,000 set aside for emergencies. This can cover some deductibles and household emergencies. Over time, I recommend saving 3-6 months of expenses as an emergency fund.

High-Interest Credit Card Debt

If you are paying high-interest credit card debt, you’re paying more in interest than you’ll be making in interest in the stock market.

For example, the average interest payment on a credit card last year was 15.91%! Making that much in the stock market consistently is very unlikely to happen, but you are guaranteed to SAVE that amount by paying off your credit card debt.

For that reason, I wouldn’t suggest investing in the stock market until you are credit card debt-free. That doesn’t mean you have to cut up your credit cards, but you need to be paying them off in full every month, no matter what.

How to Get Started With Investing

Perhaps I’ve convinced you that investing now is a good idea. Great! You mentioned a Roth IRA and that is a great place to invest.

What is so excellent about a Roth IRA?!

For starters:

- This retirement account grows tax-free.

- You can withdraw 100% of your contributions at any time without penalties or taxes.

- Your options for investing are plentiful including mutual funds, bonds, and real estate.

- Index investors who are working toward FIRE also really tend to love Roth accounts!

Speaking of index investing, that is my preferred way to invest especially when it comes to a Roth IRA. You get excellent diversification, low fees and your funds are self-cleansing. When one company isn’t performing well, it gets kicked out of the index and you don’t need to adjust anything.

If you’re looking for a partner to start your Roth IRA, I’d suggest M1 Finance. You’ll hear more about them in a moment.

Outside of the Roth IRA, THE best place to start when it comes to investing for your retirement is with employer matching funds in a 401k or 403b because that is free money!

For example, let’s say your company matches 50% of your contributions per year up to your first $5,000 of contributions. If you decide to do $5,000 of contributions, then your company will also contribute another $2,500. That’s $2,500 of free money.

Some companies are also doing this with their Health Savings Accounts (HSA) programs as well. If you contribute to your HSA, they may match a portion of your contributions.

Check with your company to see what matching benefits they provide for your retirement and your future health care costs. There may be some FREE money lying around waiting for you to snag it.

Final Thoughts: Is Now a Good Time to Invest?

Timing the market is a game most everyone will lose. Time in the market is easier and more effective.

When markets go up, people can tend to buy more shares. And when markets go down (like it has this year so far), people tend to sell more shares.

This is the opposite of what we should do right?!

Well, why do we do this?

It’s because we’re emotional beings. We’re illogical at times. We are HUMAN!

That’s why I like to take the logic and reasoning out of my hands and automatically put the same amount in my account each month no matter what.

That way, no matter what happens, I’m building wealth and keeping my emotional self away from my money. And I’d suggest the same for you.

Are you wondering “is now a good time to invest”? Are you waiting or investing?

Please let us know in the comments below.